* Note: Use the Referral Code (GWT5WBUK) when signing up to earn a free S$10 FairPrice E-Voucher!

Trust Bank is a fully online digital bank in Singapore backed by Standard Chartered and FairPrice Group (also commonly known as NTUC). They offer various products such as credit and debit cards, savings accounts, as well as various discounts and promotion rewards such as earning Linkpoints to spend at NTUC FairPrice supermarkets.

How to Use Trust Bank Referral Code

It is very simple to use the Trust Bank referral code. Firstly, sign up at the official Trust Bank website and download the Trust App following the instructions.

When signing up, be sure to enter the referral code (GWT5WBUK) during the signup process. The referral code can be inputted right at the start of the signup process, after clicking “Get started” on the app.

Benefits of Trust Bank Referral Code

The benefit of using the Trust Bank referral code is earning a $10 NTUC FairPrice E-Voucher, which can be used at NTUC FairPrice supermarkets all over Singapore.

Hence, it is important to enter the referral code during the signup process in order to avoid missing out on the promotion benefit of the $10 NTUC voucher.

Trust Bank Review

One big advantage of Trust Bank is that it is fully digital. There is no need to step into a physical bank branch during the signup process, everything can be done from the comforts of the user’s home.

In addition, the credit card and debit card of Trust Bank has strong benefits when buying at NTUC FairPrice supermarkets. For example, there can be up to 21% savings when shopping at NTUC FairPrice supermarkets.

For Trust Bank’s savings account, the interest is decent at 2.5% p.a., though not fantastic considering many alternative banks can offer higher interest rates.

In conclusion, Trust Bank is a great digital bank to signup for customers of NTUC FairPrice supermarkets, due to the high discount rates offered. Even for non-NTUC customers, they can sign up for free just to get the referral code’s NTUC E-voucher rewards.

Trust Bank Invitation Code / Promo Code

Once again, if you decide to sign up for Trust Bank, do use the invitation code “GWT5WBUK” when prompted.

Disclaimer: The opinions on Trust Bank expressed in this blog post are for general informational purposes only and are not intended to provide specific advice or recommendations for any individual or on any specific security or investment product. It is only intended to provide information on Trust Bank Referral Code. In particular, this blog post is not a substitute for obtaining advice from a qualified investment advisor.

The below YouTube video is an informative introduction and review of Trust Bank.

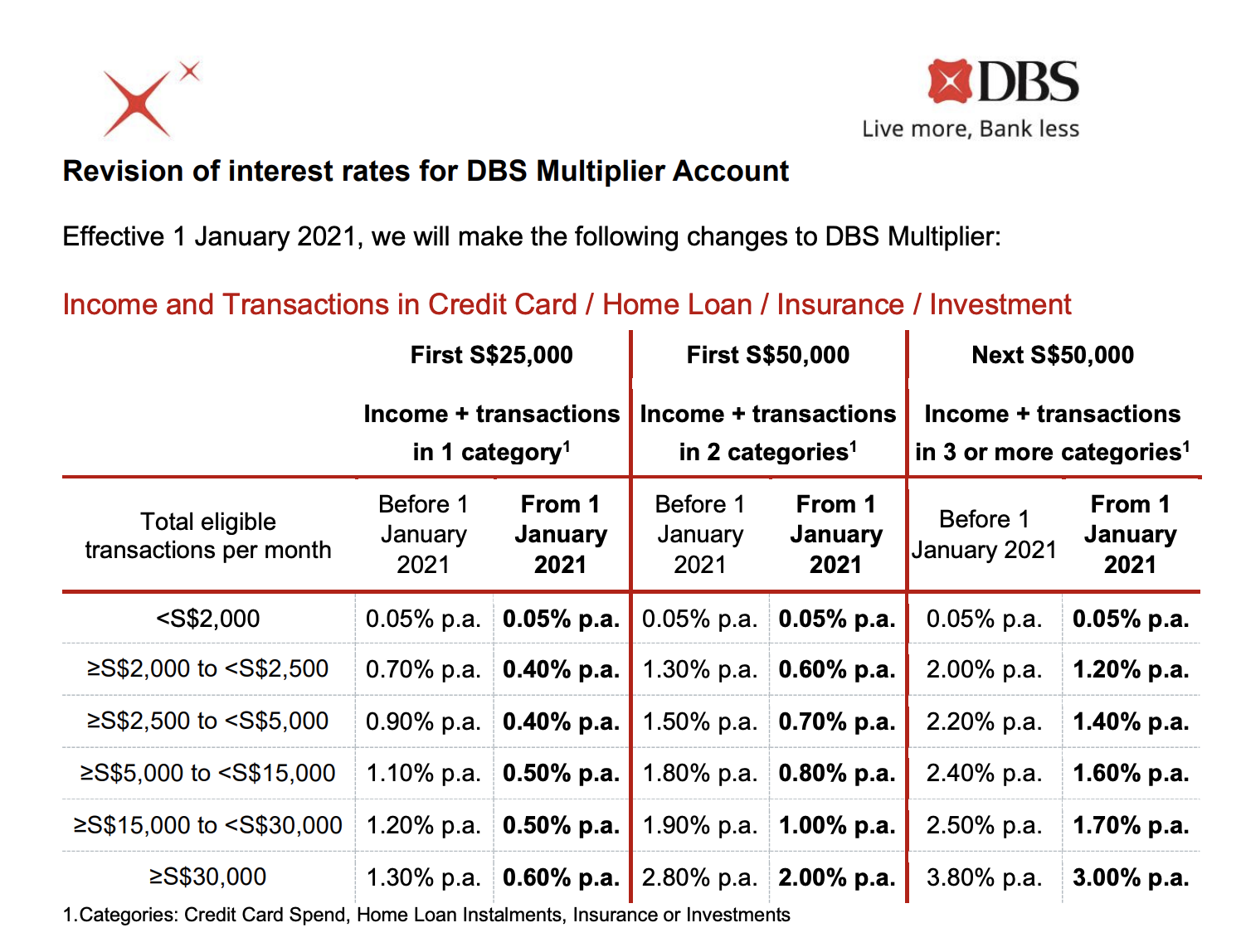

DBS Multiplier has officially announced some changes, effective 1 January 2021. Do check out the official PDF document here.

We also attach the screenshot below for the reader’s convenience.

DBS Multiplier Review

Well, it is clear that the DBS Multiplier changes are not good! Most of the interest rates are heavily affected, especially for the average Singaporean saver. This is not unique to DBS though, most banks in Singapore have slashed their interest rates, including Citibank, CIMB, and others.

For savers who have less than 3 categories transactions (Credit Card Spend, Home Loan Instalments, Insurance or Investments), most likely his/her interest rate will drop to below 1% p.a. This is a halving of the previous interest rate.

DBS Multiplier Minimum Balance

Note that DBS Multiplier has a relatively high minimum balance of S$3,000, and there is a service charge of S$5 if average daily balance falls below S$3,000.

DBS Multiplier Alternative

If you are looking for an alternative to DBS Multiplier, do check out our previous blog post Gigantiq Promo Code: MATH88. Basically, Gigantiq is a capital guaranteed savings plan that offers interest rate of 1.8% p.a. (previously 2% p.a.). This is much higher than all banks currently, including fixed deposits. Gigantiq is backed by Etiqa, which is the insurance branch of Maybank, the largest bank in Malaysia.

Update: Instead of Singlife, we now recommend GIGANTIQ. Do check out our blogpost on GIGANTIQ (2% p.a. interest and up to 8% PolicyPal bonus credits earnings).

Previously, we have written on Singlife Review before, just to update and give more details on the excellent Singlife 2.5% interest account and give an in-depth review.

Basically, Singlife’s 2.5% interest is the highest among all deposit accounts in Singapore as of September 2020. (If you know of any higher interest rate accounts, do comment below!)

Also, Singlife’s 2.5% interest does not require you to do any credit card spendings, nor do you need to credit your salary, nor purchase any insurance or investments (unlike DBS Multiplier or OCBC 360 account). Basically, you need to do nothing!

If you put in $10,000 into Singlife (which is the recommended amount to put in), it is a free $250 for you within one year. For amounts greater than $10,000, it is recommended that you put the rest into Dash EasyEarn.

In conclusion, due to reduction of interest rates in banks, currently there is no bank account (be it savings or even fixed deposit) that can beat or even come close to Singlife’s 2.5% interest. (Unless you can fulfill multiple conditions in DBS Multiplier.)

Hence, Singlife’s 2.5% interest rate is very attractive currently!

I’ve had a great experience with the Singlife Account, an insurance savings plan, and thought you would love it too! Save, spend, earn, & be insured! Install the app and sign up today to begin earning up to 2.5% p.a.* returns with your savings.

In order to use Dash EasyEarn, you first need to have Singtel Dash. The referral code is below!

Hi, we’re giving you up to $2 cashback for your first Singtel Dash transaction! Sign up with the referral code DASH-2I2KM or tap on this link https://appserver.dash.com.sg:443/mgm?DASH-2I2KM now. T&Cs apply.

Singtel Dash EasyEarn Review

We will give a short review of Singtel Dash EasyEarn. Technically, Dash Easy Savings Account is a insurance policy, but it works like a bank savings account. Basically the pros and cons of Singtel Dash EasyEarn are as follows.

Pros:

2% per annum interest (much better than bank savings account or even fixed deposit).

This 2% holds for deposits up to $20,000.

Capital-guaranteed.

Protected by SDIC.

No lock-in period.

Comes bundled with life insurance (Be automatically covered with a death benefit of 105% of your Account Value).

Singtel is a big company (one of the biggest in Singapore), with good reputation and long history.

Cons:

There is a $0.70 fee for withdrawing to bank account (quite a low fee though).

Minimum balance of $2000 in order to earn the max 2% interest (quite a low requirement).

The 2% interest rate is only guaranteed for the first policy year.

The insurance policy is actually administered by Etiqa, not Singtel. Etiqa is a big insurance company though, it is part of Maybank which is the biggest bank in Malaysia.

I tried the transfer of funds into Dash EasyEarn (it is by eNETS only). The speed is very fast, almost instantaneously I could see the funds in Dash EasyEarn after transferring. I have not tried withdrawal of funds yet, due to the $0.70 withdrawal fee.

Update September 2020: I tried withdrawing, the process was very smooth and instantaneous. Basically, the withdrawal is via PayNow to the bank account linked to your mobile number. Your bank account will receive the amount withdrawn within seconds, while the $0.7o withdrawal fee is deducted from your Dash EasyEarn balance.

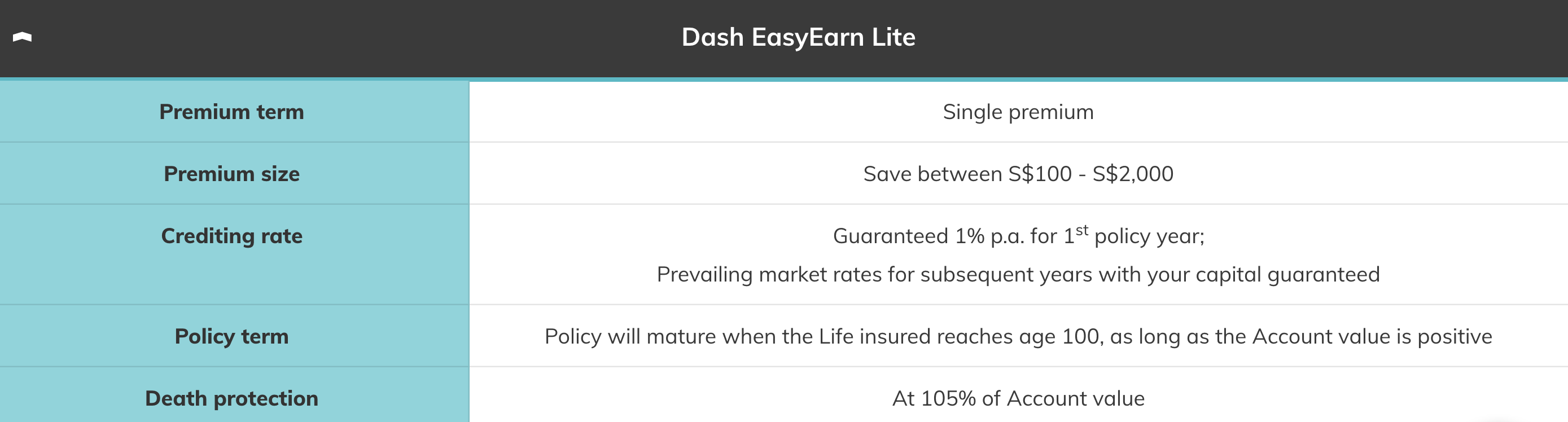

Dash EasyEarn Lite

What is this Dash EasyEarn Lite? Apparently, it is the “small” version of Dash EasyEarn when you deposit $2,000 or less. The interest rate is also correspondingly lower, at 1%.

Update: The above information is incorrect. An official Singtel representative has contacted us to tell us the correct information.

The Dash EasyEarn Lite option is not automatically applied when the savings amount is less than $2,000 as it is only open to eligible Dash users such as work permit holders.

Is Dash EasyEarn Safe?

A popular question asked is definitely whether Dash EasyEarn is safe? The answer is it is safe.

Secondly, Dash EasyEarn is a capital-guaranteed savings insurance policy. That means, it is impossible to lose the principal amount you put in. For example, if one puts in a capital of $20k (the max amount allowed), one will get back at least $20k no matter what the circumstances.

Lastly, Etiqa (the insurance company behind Dash EasyEarn) is regulated by Monetary Authority of Singapore (MAS). Their MAS license can be found on the MAS official website.

Basically, Singlife offers a higher interest rate of 2.5%, however this only applies to your first $10k deposit. Even though Dash EasyEarn offers a lower interest rate of 2%, it applies to a higher amount of $20k.

A logical conclusion is to max out Singlife first (by putting $10k in Singlife). Then, put in your excess in Dash EasyEarn.

(The Singlife referral code/ promo code is the above URL link. Just click it on your mobile device to apply the referral code.)

Dash EasyEarn Forum

If you still have any doubts about Dash EasyEarn, a good way to dispel your doubts is to read forums on Dash EasyEarn. The best forum on Dash EasyEarn is the one in HardwareZone Money Mind. The experts there will teach you more on how to maximize your earnings using Dash EasyEarn.

Disclaimer: The opinions on Dash EasyEarn Account expressed in this blog post is for general informational purposes only and are not intended to provide specific advice or recommendations for any individual or on any specific security or investment product. It is only intended to provide information on Dash EasyEarn Referral and Dash EasyEarn Review. In particular, this blog post is not a substitute for obtaining advice from a qualified investment advisor.

Update: Instead of Singlife, we now recommend GIGANTIQ. Do check out our blogpost on GIGANTIQ (2% p.a. interest and up to 8% PolicyPal bonus credits earnings).

(The Singlife referral code/ promo code is the above URL link. Just click it on your mobile device to apply the referral code.)

If you install and apply for Singlife using the above Singlife Referral Code, you will get S$10 credited to your Singlife account, as soon as you set up your Singlife account and activate your free Singlife Visa debit card.

Singlife Review

Singlife is a insurance savings plan that works similarly to a bank account, providing you a 2.5% per annum interest. You may withdraw your savings at any time, there is no lock in period.

What is most attractive about Singlife is definitely the 2.5% interest, it currently much better than many banks’ savings account or even fixed deposit account.

I find the setting up process very easy, it should take less than 15 minutes and can be done entirely online. The app is quite intuitive to use, and has a clean user-friendly interface.

I have personally tested the Singlife withdrawal (withdraw from the Singlife bank to a DBS bank account). While it is not instantaneous, the withdrawal is very fast (around 5 minutes to appear in my bank account). On paper, it can take up to 3 hours for the Singlife withdrawal process, which is still quite acceptable.

Singlife Protected by SDIC and Capital Guaranteed

One question that is bound to be asked by Singaporeans is “Is Singlife safe?”. Or “Is it safe to put my money in Singlife?”.

In addition, the Singlife Account is capital guaranteed, which means that the principal amount you put in is shielded from any losses (unlike stocks where you can lose your capital).

Lastly, Singlife is regulated by Monetary Authority of Singapore (MAS). Their MAS license can be found on the MAS official website.

So let us summarize the pros and cons of Singlife account.

Pros:

High interest of 2.5% p.a. (No other bank has such a high interest at the time of writing this post, even fixed deposits cannot compare with Singlife.)

Capital-guaranteed.

Protected by SDIC.

Comes bundled with life insurance and retrenchment insurance.

Comes with free Visa card (no fees).

Cons:

The 2.5% interest rate is not guaranteed (it can go up or down in the future). According to the Singlife Facebook, it will uphold the interest rate for at least a year.

The 2.5% interest rate is only for the first $10k in your Singlife Account. Subsequently amounts above your first S$10,000 up to S$100,000 will earn 1% p.a. returns (which is still quite good). Amounts above S$100,000 will not earn any returns.

No ATM machines, it is totally virtual.

Singlife is still relatively not well-known at the moment.

Singlife Hardwarezone and Singlife Reddit

You can check out the discussion about Singlife on the popular forum Hardwarezone or Reddit.

Basically, the comments about Singlife are quite positive (especially regarding the high 2.5% interest). The sentiment is that there is no harm trying out Singlife (while the high 2.5% interest is active, and then reconsider or transfer out when the interest rates drop).

If you decide to sign up with Singlife, do so with the referral code link below, and get $10 credited to your account!

The Singlife Account comes with a free Visa Debit Card. It has no annual fees and no FX (foreign exchange) fees. You can use the Singlife Debit Card overseas, there will be zero FX fees imposed on your overseas purchases.

Even if you just intend to use it rarely, there is no harm just activating your Singlife Debit Card. You can get instant notifications on your spending in the Singlife App. For greater security, you can lock and unlock your Singlife Card all through the Singlife App.

The most important thing to note regarding Singlife Debit Card is that you must activate it in order to get the S$10 Referral or Promotion bonus.

Disclaimer: The opinions on Singlife Account expressed in this blog post is for general informational purposes only and are not intended to provide specific advice or recommendations for any individual or on any specific security or investment product. It is only intended to provide information on Singlife Referral and Singlife Review. In particular, this blog post is not a substitute for obtaining advice from a qualified investment advisor.

Just received the following official notice (from Citibank Estatement):

With effect from 2 December 2019, the base interest rate for the Citi MaxiGain Savings Account will be revised to 50% of the 1-month Singapore Dollar Interbank Offer Rate (1-month SIBOR). The bonus interest rate will also be revised to step up monthly from 0.05% p.a. to a maximum of 0.60% p.a.. You may refer to http://www.citibank.com.sg/maxigaintcdec2019 for more information.

I think basically this spells the end of the wonderful Citi MaxiGain Savings Account, especially if you are depositing less than $70k SGD, whereby one will only get the bonus interest rate of maximum 0.60% p.a.

A possible alternative that I am currently considering is ICBC Fixed Deposit, which gives an interest rate of 1.85% p.a., more than triple that of the new Citi MaxiGain Account.

Basically, for accounts below S$70,000, the maximum interest rate is now 1.2% provided there are no withdrawals. Hence, effectively it is like a Fixed Deposit with 1.2% interest with the slight benefit that you can still perform withdrawals if you want, but the interest rate drops to 0.6% (6 counters).

Previously, the interest rate was exceptionally fantastic at around 2.2% (depends on the SIBOR rate). This fantastic rate is still available for amounts of S$70,000 and above.

Possibly a short term fixed deposit like CIMB or ICBC may be a better choice now, for amounts below S$70,000. Both CIMB and ICBC have offers of around 1.9% interest rate for their fixed deposits.

Albert Einstein once said that “Compound interest is the eighth wonder of the world. He who understands it, earns it … he who doesn’t … pays it.”

In E Maths, students will learn that the formula for Compound Interest is . The exponential “to the power of n” explains the powerful effect of compound interest.

Choosing the right savings account can earn you hundreds of dollars or more per year (depending on how much savings you have).

There are many savings accounts that require a lot of “action” on your part, notably you need to credit your salary (with SAL code) to the bank, use their card, buy their investment/insurance/loan products, etc. These accounts include DBS Multiplier, OCBC 360, BOC Smart Saver, etc.

However, many people may not meet their criteria (or may not want to use so much of their products). For instance, self-employed people may not have SAL code salary.

Currently, I think the 2 best “Do-nothing” saving accounts in Singapore are:

Citi MaxiGain

From Citibank, the interest rate of MaxiGain is tied to the SIBOR rate. Starting interest will be 80% of SIBOR, stepping up 0.1% for 12 counters. Final rate is around 2% or more. This is frankly better than many fixed deposits. The only downside is that if you withdraw from the account, the counter will drop to 0 (or to 6 once you reach the checkpoint of 6 counters). But even with the counter dropping to zero, the interest is around 0.8% or more which is pretty decent.

Citibank is a very reliable bank from America, with bigger market capital than DBS. Tip: According to online sources, your account may be temporarily “frozen” for inactivity if you don’t have any transaction for too long a period. Hence, it is recommended to set up an automatic credit of $1 monthly to your Citibank Maxigain account.

CIMB FastSaver Account

Most people would not have heard of CIMB bank. It is a Malaysian bank. Not to worry though, they are listed under Singapore Deposit Insurance, that means you are insured up to $50,000 even if something bad happens to the bank. CIMB FastSaver is quite amazing in that it gives 1% interest, with no minimum balance or penalty for withdrawing. That means you can withdraw as and when you like. Their account is entirely online, you don’t have to step into their branch even for creating your account. It is a simple and effective savings account.

. The exponential “to the power of n” explains the powerful effect of compound interest.

. The exponential “to the power of n” explains the powerful effect of compound interest.